When tenants negotiate an office lease, most of the focus naturally goes toward the big-ticket items like:

- Rental rate

- Free rent

- Tenant improvement allowance

- Lease term

Those items are easy to see and easy to compare but what often receives far less attention in many office leases is Additional Rent.

Additional Rent can substantially increase occupancy costs over the life of a lease therefore it's crucial to understand those costs, as well as identify where there may be opportunities to negotiate limits to its exposure.

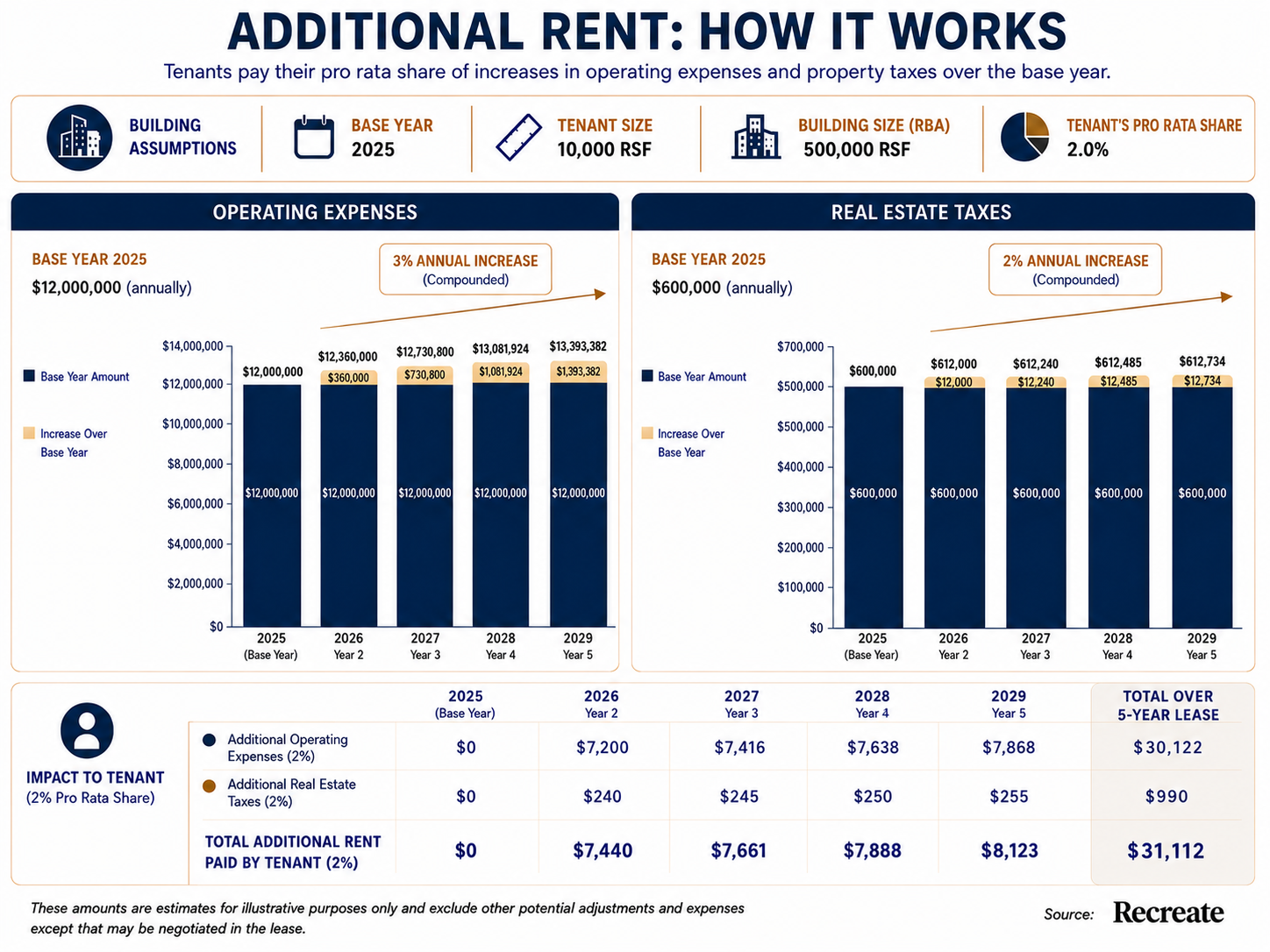

What Is Additional Rent?

In most multi-tenant office buildings, tenants pay two forms of rent:

Base Rent: This is the fixed rental rate stated in the lease.

Additional Rent: This is the tenant's share of increases in operating expenses, insurance and property taxes above a specified base year.

The "Base Year"

Most office leases use a "Base Year" structure, which is typically the year that you move in, though it could be set to the following year if you take occupancy in the second half of the year.

The landlord then establishes the building's operating expenses and real estate taxes during a specific calendar year.

For example:

- Lease Commencement: January 1, 2026

- Base Year: 2026

- Building Operating Expenses in 2026: $18.00 per square foot

If operating expenses increase to $19.00 per square foot in 2027, tenants pay their proportionate share of the $1.00 increase.

Therefore, if you occupy 10% of the building, you'd be responsible for $0.10 per square foot (10% of the $1.00/SF increase).

Why Historical Expenses and Assessed Value Matter

Before signing an office lease, the tenant's real estate representative should obtain the property’s historical operating expenses and understand the building’s current assessed value.

Historical operating expenses show how the building has actually performed over time. If expenses have increased 3% annually for the last several years, that tells one story. If they jumped 18% last year because of insurance, security, utilities, repairs, or management fees, that tells a very different story.

The goal is to understand whether future increases are likely to be modest, predictable, or painful.

Property taxes deserve the same attention. In California, a building’s assessed value can have a major impact on future tax pass-throughs. If the property was recently sold, refinanced, reassessed, or is likely to sell during your lease term, real estate taxes may increase significantly.

If the building sells during your tenancy and is reassessed at a substantially higher value, the impact could be significant as those increases in taxes are passed through to the tenants. While negotiating a cap on this exposure is not an option for most tenants, understanding this potential risk BEFORE signing a lease is crucial.

Sophisticated tenants should review:

- At least three years of historical operating expenses

- Historical property tax bills

- The current assessed value of the property

- Whether the property has recently sold or may be sold

- Any major capital projects, insurance increases, or service cost changes

- The lease language governing tax increases and operating expense exclusions

The purpose is not just to understand what the building costs today. It is to understand what the building may cost over the full lease term.

The "Gross-Up" Clause

One of the most misunderstood provisions in office leases is the expense "gross-up."

Imagine a building is only 50% occupied when you move in, therefore since fewer tenants are occupying the building, certain variable expenses such as utilities, consumables and janitorial services will be lower than if the building were full.

To protect tenants from rising occupancy costs due to rising occupancy, landlords often "gross up" these expenses to reflect what they would have been if the building were fully occupied (typically 95 - 100%).

Therefore if the water bill doubles when the building increases from 50 to 100% occupancy, tenants are shielded from paying their pro-rata share of that increase.

Make sure this clause is in your lease if your lease is structured to pass through increases in operating expenses.

Negotiation Opportunities

Many tenants assume operating expense pass-throughs are non-negotiable and are often surprised to learn that significant protections can be negotiated, such as:

- Caps on controllable operating expense increases

- Exclusions for capital expenditures

- Limits on management fees

- Restrictions on administrative markups

- Audit rights

- More favorable gross-up language

These provisions may not generate the same excitement as free rent or tenant improvements, but they can create substantial savings over time.

Final Thoughts

Additional Rent projections rarely receive the attention they deserves, but when it comes to long-term occupancy cost planning they should absolutely be part of the analysis.

The most sophisticated tenants don't just negotiate rent, they negotiate the total cost of occupancy.

If you're evaluating a lease renewal, relocation, or expansion, make sure you're looking beyond the rental rate. Understanding how Additional Rent works today can help avoid expensive surprises tomorrow.